Home >> Blog >> Banking Liquidity Crisis | Its Impact on Banks and Economy

Banking Liquidity Crisis | Its Impact on Banks and Economy

Table of Contents

We often discuss the possibility of a recession in the US economy, but have you ever considered that a similar downturn could happen in India? Or have have you ever thought about the impact of declining bank deposits and casa ratio on Indian economy? Our economy isn't immune to significant challenges, and recent trends suggest that we could be heading toward a scary situation.

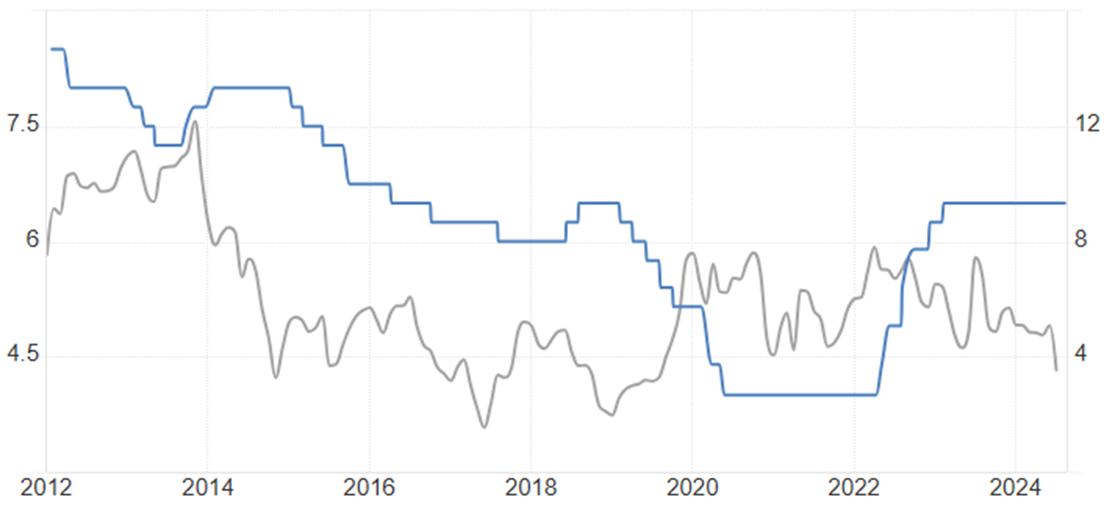

RBI Governor, Mr. Shaktikanta Das, has highlighted a concerning trend—Instead of depositing money into banks, people are seeking alternative investment avenues. This shift has led to a significant decline in the credit-to-deposit ratio, which is an alarming signal for both the banking sector and the overall economy.

While this trend is clearly negative for banking stocks, it also casts a shadow on the broader Indian economy.

Why Are Bank Deposits Declining?

For frequent depositors, bank deposit rates are between 2.50% and 9% for terms ranging from 7 days to 10 years. But this is not the case now. For this, we need to look at the relationship between Bank FD rates and inflation.

Between the years 2020 to 2022, inflation was higher than interest rates, which forced people to withdraw their deposits. Now, the question arises—where is that money being invested?

Detailed Video:

There are four major avenues where this money is being redirected:

-

Mutual Funds

-

Stock Market

-

Gold

-

Real Estate

These areas are driven by higher returns compared to bank interest rates. This explains the decline in bank deposits and where the money is going.

CASA Deposit Trend:

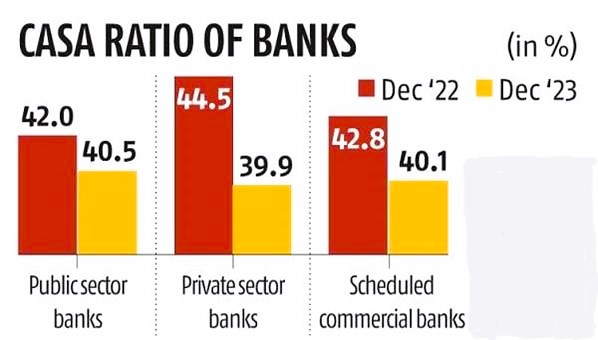

The SBI study also noted that as savings bank deposits decreased, CASA (Current Account Savings Account) deposits decreased, from 43.5% in the prior year to 41% in the financial year 2024.

According to the data, the reduction in savings bank deposits is in line with the 42% pre-COVID-19 pandemic levels and indicates a change in the way the money are being utilized.

Because savings bank deposits are mostly utilized for transactions, which cause more movement within the financial system, their stability is a cause for concern.

The Impact on Banks and the Economy

So how this impacts banks and why it poses a risk to the Indian economy?

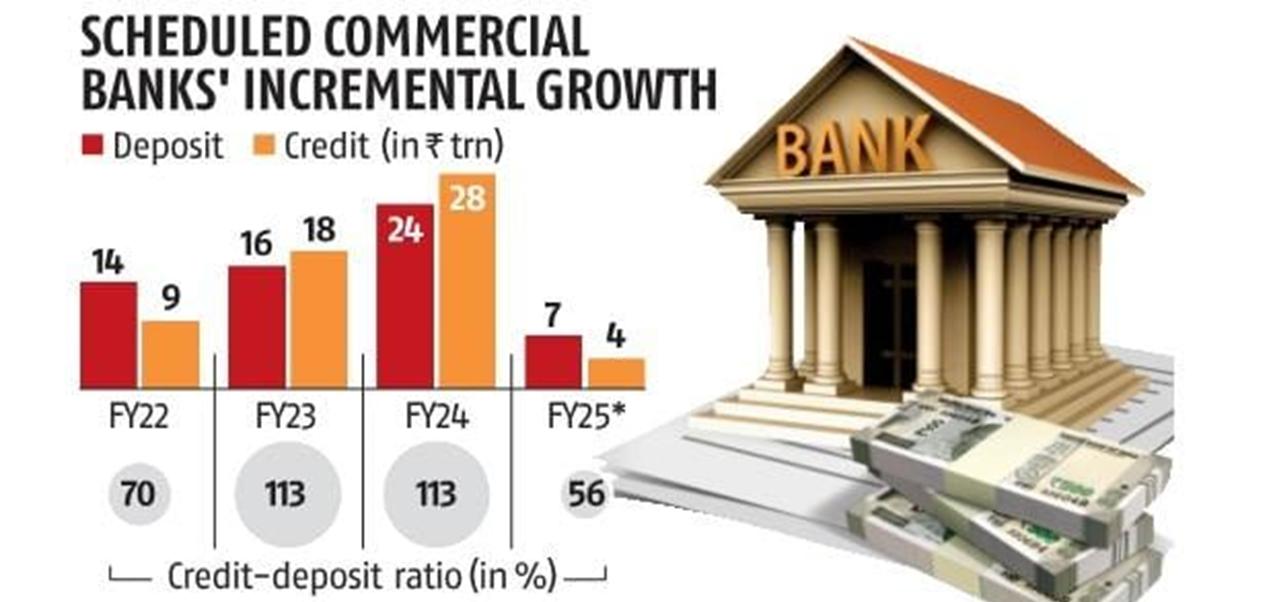

Banks primarily function by taking deposits from individuals and offering them a return of 5-6%. They then lend this money to companies, corporate houses, and other entities, charging them 9-10%. This difference, known as the Net Interest Margin (NIM), is the bank's primary source of income.

Previously, this model worked well. But now it has reversed. while deposits have decreased, credit (loans) have surged.

This explains why banks are currently facing significant challenges. This situation can also be analyzed through the CASA ratio, which measures the proportion of a bank's deposits in current and savings accounts. This data provides additional insight into the decline in bank deposits compared to current accounts.

The Broader Economic Implications

So, how can this situation harm the entire economy? Imagine if banks continue to see a decline in deposits, eventually exhausting their reserves and becoming unable to lend. What if you go to the bank, with a good CIBIL score, asking for a Rs.20 lakh loan, only to be told that the bank has no money to lend?

If banks start refusing loans to people like us, it will lead to a drop in consumption, as we won't be able to finance your planned expenditures. A decline in consumption will, in turn, negatively impact the entire economy.

For India, this is particularly concerning because consumption accounts for 55-60% of GDP. Just imagine the potential damage this could cause—a vicious cycle where every part of the economy is interconnected, and a failure in one area could disrupt the entire system.

This is why the RBI Governor has emphasized the importance of increasing bank deposits and urged both individuals and banks to adopt measures that encourage savings.

Conclusion

In summary, the decline in bank deposits and shifts in the CASA ratio pose a major challenge for the Indian economy. As money moves away from traditional deposits to alternative investments, banks face a reduced pool of funds to lend, which impacts their income and restricts credit access. This reduction in consumption can harm India's GDP and destabilize the economy. To address these risks, it's vital for individuals and banks to maintain healthy deposit levels and encourage balanced investments to support economic stability and growth.

Disclaimer: The content is purely for educational and information purposes only. We do NOT encourage/advise/suggest our active readers to be involved in any kind of buying or selling securities activities. Always consult your eligible financial advisor for investment-related decisions.

Frequently Asked Questions

The CASA (Current Account Savings Account) ratio measures the proportion of a bank's deposits held in current and savings accounts. A high CASA ratio indicates that a bank has a lower cost of funds, as these accounts typically offer lower interest rates. This is important for banks because it helps them maintain profitability while providing loans at competitive rates.

Bank deposits in India are declining due to several factors, including low-interest rates on fixed deposits, rising inflation, and the availability of higher returns from alternative investment options like mutual funds, the stock market, gold, and real estate. This shift in investment preferences has led to reduced inflows into traditional bank deposits.

A declining CASA ratio can have significant implications for the Indian economy. It reduces banks' ability to lend at competitive rates, which can restrict access to credit for businesses and consumers. This, in turn, can slow down economic growth by reducing consumption and investment, both of which are critical drivers of the economy.

Declining bank deposits can lead to a reduced pool of funds available for lending, making it harder for individuals and businesses to obtain loans. This can result in lower consumption, reduced business investment, and ultimately, a slowdown in economic growth. In the long run, this could affect the overall stability of the Indian economy.

To address the decline in bank deposits, it is important to offer more attractive interest rates on deposits, encourage savings, and create awareness about the importance of maintaining healthy deposit levels. Additionally, banks and regulators need to work together to promote balanced investments that support economic stability and growth.